A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. My Accounting Course is a world-class educational resource developed by experts to simplify accounting, finance, & investment analysis topics, so students and professionals can learn and propel their careers. Managerial accountants also use the contribution margin ratio to calculate break-even points in the break-even analysis.

- Variable expenses are costs that change in conjunction with some other aspect of your business.

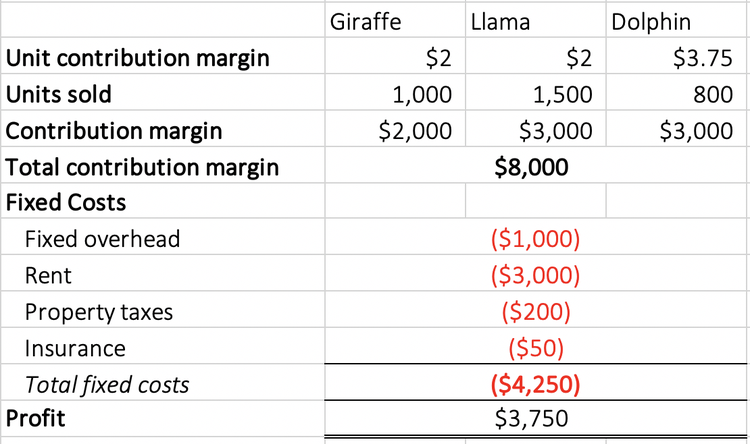

- If they send one to eight participants, the fixed cost for the van would be \(\$200\).

- In other words, your contribution margin increases with the sale of each of your products.

What does a high or low Contribution Margin Ratio mean for a business?

Management accountants identify financial statement costs and expenses into variable and fixed classifications. Variable costs vary with the volume of activity, such as the number of units of a product produced in a manufacturing company. The contribution margin ratio is the difference between a company’s sales and variable costs, expressed as a percentage. This ratio shows the amount of money available to cover fixed costs. It is good to have a high contribution margin ratio, as the higher the ratio, the more money per product sold is available to cover all the other expenses.

How Do You Calculate the Contribution Margin?

When it splits its costs into variable costs and fixed costs, your business can calculate its breakeven point in units or dollars. At breakeven, variable and fixed costs are covered by the sales price, but no profit is generated. You can use contribution margin to calculate how much profit your company will make from selling each additional product unit when breakeven is reached through cost-volume-profit the 16 best marketing strategies for small businesses analysis. At a contribution margin ratio of \(80\%\), approximately \(\$0.80\) of each sales dollar generated by the sale of a Blue Jay Model is available to cover fixed expenses and contribute to profit. The contribution margin ratio for the birdbath implies that, for every \(\$1\) generated by the sale of a Blue Jay Model, they have \(\$0.80\) that contributes to fixed costs and profit.

What Is the Difference Between Contribution Margin and Profit Margin?

While contribution margin is expressed in a dollar amount, the contribution margin ratio is the value of a company’s sales minus its variable costs, expressed as a percentage of sales. However, the contribution margin ratio won’t paint a complete picture of overall product or company profitability. If you need to estimate how much of your business’s revenues will be available to cover the fixed expenses after dealing with the variable costs, this calculator is the perfect tool for you. You can use it to learn how to calculate contribution margin, provided you know the selling price per unit, the variable cost per unit, and the number of units you produce. The calculator will not only calculate the margin itself but will also return the contribution margin ratio.

Step 3 of 3

The 60% CM ratio implies the contribution margin for each dollar of revenue generated is $0.60. If the contribution margin is too low, the current price point may need to be reconsidered. In such cases, the price of the product should be adjusted for the offering to be economically viable. The companies that operate near peak operating efficiency are far more likely to obtain an economic moat, contributing toward the long-term generation of sustainable profits. Management should also use different variations of the CM formula to analyze departments and product lines on a trending basis like the following. As a manager, you may be asked to negotiate or talk with vendors and perhaps even to ask for discounts.

To convert the contribution margin into the contribution margin ratio, we’ll divide the contribution margin by the sales revenue. If the total contribution margin earned in a period exceeds the fixed costs for that period, the business will make a profit. If the total contribution margin is less than the fixed costs, the business will show a loss. In this way, contribution margin becomes an important factor when calculating your break-even point, which is the point at which sales revenue and costs are exactly even ($0 profit). This, in turn, can help you make better informed pricing decisions, but break-even analysis won’t show how much you need to cover costs and make a profit.

As with other figures, it is important to consider contribution margins in relation to other metrics rather than in isolation. Profit margin is calculated using all expenses that directly go into producing the product. The contribution margin shows how much additional revenue is generated by making each additional unit of a product after the company has reached the breakeven point. In other words, it measures how much money each additional sale “contributes” to the company’s total profits. The addition of $1 per item of variable cost lowered the contribution margin ratio by a whopping 10%.

On the other hand, net sales revenue refers to the total receipts from the sale of goods and services after deducting sales return and allowances. As you can see, the net profit has increased from $1.50 to $6.50 when the packets sold increased from 1000 to 2000. However, the contribution margin for selling 2000 packets of whole wheat bread would be as follows. Remember, that the contribution margin remains unchanged on a per-unit basis.

One of the important pieces of this break-even analysis is the contribution margin, also called dollar contribution per unit. Analysts calculate the contribution margin by first finding the variable cost per unit sold and subtracting it from the selling price per unit. Contribution margin, gross margin, and profit are different profitability measures of revenues over costs.

For variable costs, the company pays $4 to manufacture each unit and $2 labor per unit. The contribution margin income statement separates the fixed and variables costs on the face of the income statement. This highlights the margin and helps illustrate where a company’s expenses. Variable expenses can be compared year over year to establish a trend and show how profits are affected. The difference between the selling price and variable cost is a contribution, which may also be known as gross margin.

This cost of the machine represents a fixed cost (and not a variable cost) as its charges do not increase based on the units produced. Such fixed costs are not considered in the contribution margin calculations. The contribution margin is computed as the selling price per unit, minus the variable cost per unit. Also known as dollar contribution per unit, the measure indicates how a particular product contributes to the overall profit of the company. More specifically, using contribution margin, your business can make new product decisions, properly price products, and discontinue selling unprofitable products that don’t at least cover variable costs. The business can also use its contribution margin analysis to set sales commissions.